The Changing Landscape of Insurance

Insurance has always been the backbone of global economies, providing financial stability and protection against uncertainties. Yet, insurers have historically been cautious, prioritizing solvency and underwriting margins over modernization. This conservative approach has often slowed innovation, leaving the industry struggling to cope with sudden spikes in risks such as climate-related losses, inflation, and geopolitical instability.

In 2024, many carriers resorted to short-term fixes like raising premiums or withdrawing from high-risk markets. While this boosted short-term profitability—delivering the strongest results for property and casualty (P&C) since 2007 and record annuity sales—the long-term outlook requires a shift. In 2025, insurers must accelerate transformation, embed technology at scale, and rebuild customer trust to remain relevant in a fast-changing world.

2025 Global Insurance Outlook: Adapting to Rapid Change

Consumers today are empowered by digital tools, particularly generative AI, and expect personalized, transparent, and accessible insurance products. Insurers can no longer rely solely on backward-looking risk models. Modernizing infrastructure, adopting advanced risk assessment tools, and streamlining operations are becoming central to building resilience.

Maintaining trust will be crucial. After years of premium hikes and reduced coverage, consumers demand fairness, transparency, and inclusivity. Regulators are also pressing insurers to disclose climate-related risks and make insurance affordable for vulnerable communities.

Partnerships with insurtechs and technology vendors will likely accelerate innovation, offering carriers faster and more flexible solutions without the heavy burden of building everything in-house.

Non-Life Insurance: Profitability and Emerging Risks

The non-life sector rebounded strongly in 2024, posting a US$9.3 billion underwriting gain in the US alone. Improved combined ratios and investment income boosted overall profitability. However, challenges remain.

-

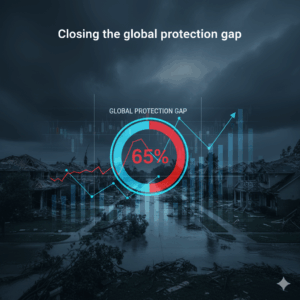

Catastrophe losses: Global insured losses exceeded US$100 billion in 2023, spread across numerous smaller events. Only 35% of total economic losses were insured, highlighting a 65% protection gap.

-

Social inflation: Rising litigation costs are pushing liability reserves higher, with notable pressure in the US and Australia.

-

Geopolitical tensions: Russia-Ukraine and Middle East conflicts continue to affect cyber, marine, and political risk exposures.

Despite these challenges, premium growth, easing inflation, and higher investment yields suggest stronger profitability ahead. Non-life insurers must also prepare for emerging risks like AI liability and capitalize on opportunities in embedded insurance, a market projected to surpass US$722 billion by 2030.

Life and Annuity: Record Growth but Need for Transformation

Life and annuity (L&A) carriers have seen exceptional sales, fueled by elevated interest rates and consumer appetite for savings-linked products. In 2023, US annuity sales grew 23% to US$385 billion, while emerging markets such as China and India are driving strong premium growth.

Yet, sustainability remains a concern. Interest rate-driven demand may fade, and legacy systems hinder scalability. To thrive, L&A insurers must:

-

Modernize core systems through API-based architectures.

-

Offer predictive models to brokers and advisors for better targeting.

-

Leverage digital banking partnerships to expand access in underserved markets.

The global protection gap—US$25 trillion in US mortality coverage and US$70 trillion in retirement savings—presents massive opportunities for insurers who embrace innovation and inclusivity.

Group Insurance: Competing for Talent and Growth

Group insurers benefited from strong renewal premiums and wage inflation, but slower employment growth in 2025 could dampen results. Workplace benefits remain critical for attracting and retaining employees, with 70% of workers prioritizing strong packages.

Supplemental health and disability coverage are growing, but competition is fierce. To differentiate, group carriers are partnering with ecosystem players and insurtechs. AI-driven solutions, such as Prudential Financial’s partnership with Nayya, are helping employees make informed benefits decisions.

AI and Data: Opportunities and Challenges

AI adoption is reaching an inflection point. A Deloitte survey found 76% of US insurers have already implemented generative AI in at least one business function. Early use cases in claims, customer service, and risk management show promise, but scaling requires robust data governance and cultural buy-in.

Key considerations include:

-

Data quality and integration: Essential for reliable AI outcomes.

-

Governance and transparency: Preventing bias and building trust with regulators and consumers.

-

Talent development: Blending digital literacy with human skills like empathy and critical thinking.

AI can drive efficiency and improve both customer and employee experiences—but insurers must prioritize responsible adoption.

Balancing Profitability and Societal Purpose

Climate change, affordability challenges, and equity concerns demand insurers balance profit with purpose. Strategies include:

-

Incentivizing resilient construction with premium discounts.

-

Promoting circular economy practices, such as reusing auto parts.

-

Offering usage-based auto insurance tied to driving behavior.

-

Investing in health initiatives linked to pollution-related diseases.

Regulators are also pushing insurers to prevent bias in AI models and to disclose climate impacts in portfolios. Transparent, equitable practices will be vital for long-term sustainability.

New Global Tax Rules and Compliance Pressures

The introduction of Pillar Two global minimum tax laws, mandating a 15% minimum corporate tax rate for large multinationals, could significantly impact insurers operating in low-tax jurisdictions. Compliance, reporting, and potential restructuring will demand new investments in data and governance.

The Road Ahead: Building Resilient Operating Models

The only certainty is uncertainty. For insurers, agility, innovation, and customer focus will define success in 2025 and beyond. By embracing advanced technologies, modernizing infrastructure, and aligning profitability with societal purpose, insurers can build operating models that withstand disruption while fostering growth and inclusivity.

Stay ahead of the financial sector’s transformation—explore more insights in the top business magazine, IMPAAKT.